1. [The following information applies to the questions displayed below.]

Sweeten Company had no jobs in progress at the beginning of the year and no beginning inventories. It started, completed, and sold only two jobs during the year—Job P and Job Q. The company uses a plantwide predetermined overhead rate based on machine-hours. At the beginning of the year, it estimated that 4,000 machine-hours would be required for the period’s estimated level of production. Sweeten also estimated $25,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $1.70 per machine-hour.

Because Sweeten has two manufacturing departments—Molding and Fabrication—it is considering replacing its plantwide overhead rate with departmental rates that would also be based on machine-hours. The company gathered the following additional information to enable calculating departmental overhead rates:

| Molding | Fabrication | Total | |

|---|---|---|---|

| Estimated total machine-hours used | 2,500 | 1,500 | 4,000 |

| Estimated total fixed manufacturing overhead | $ 10,000 | $ 15,000 | $ 25,000 |

| Estimated variable manufacturing overhead per machine-hour | $ 1.40 | $ 2.20 |

The direct materials cost, direct labor cost, and machine-hours used for Jobs P and Q are as follows:

| Job P | Job Q | |

|---|---|---|

| Direct materials | $ 13,000 | $ 8,000 |

| Direct labor cost | $ 21,000 | $ 7,500 |

| Actual machine-hours used: | ||

| Molding | 1,700 | 800 |

| Fabrication | 600 | 900 |

| Total | 2,300 | 1,700 |

Sweeten Company had no overapplied or underapplied manufacturing overhead costs during the year.

Required:

For questions 1-8, assume that Sweeten Company uses a plantwide predetermined overhead rate with machine-hours as the allocation base. For questions, 9-15, assume that the company uses predetermined departmental overhead rates with machine-hours as the allocation base in both departments.

2. [The following information applies to the questions displayed below.]

Sweeten Company had no jobs in progress at the beginning of the year and no beginning inventories. It started, completed, and sold only two jobs during the year—Job P and Job Q. The company uses a plantwide predetermined overhead rate based on machine-hours. At the beginning of the year, it estimated that 4,000 machine-hours would be required for the period’s estimated level of production. Sweeten also estimated $25,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $1.70 per machine-hour.

Because Sweeten has two manufacturing departments—Molding and Fabrication—it is considering replacing its plantwide overhead rate with departmental rates that would also be based on machine-hours. The company gathered the following additional information to enable calculating departmental overhead rates:

| Molding | Fabrication | Total | |

|---|---|---|---|

| Estimated total machine-hours used | 2,500 | 1,500 | 4,000 |

| Estimated total fixed manufacturing overhead | $ 10,000 | $ 15,000 | $ 25,000 |

| Estimated variable manufacturing overhead per machine-hour | $ 1.40 | $ 2.20 |

The direct materials cost, direct labor cost, and machine-hours used for Jobs P and Q are as follows:

| Job P | Job Q | |

|---|---|---|

| Direct materials | $ 13,000 | $ 8,000 |

| Direct labor cost | $ 21,000 | $ 7,500 |

| Actual machine-hours used: | ||

| Molding | 1,700 | 800 |

| Fabrication | 600 | 900 |

| Total | 2,300 | 1,700 |

Sweeten Company had no overapplied or underapplied manufacturing overhead costs during the year.

Required:

For questions 1-8, assume that Sweeten Company uses a plantwide predetermined overhead rate with machine-hours as the allocation base. For questions, 9-15, assume that the company uses predetermined departmental overhead rates with machine-hours as the allocation base in both departments.

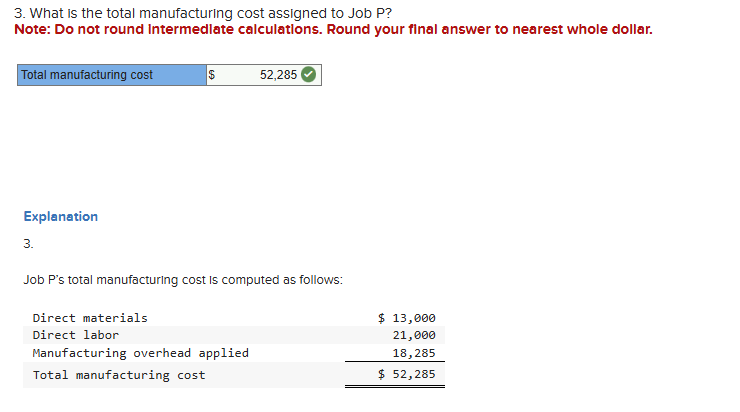

3. [The following information applies to the questions displayed below.]

Sweeten Company had no jobs in progress at the beginning of the year and no beginning inventories. It started, completed, and sold only two jobs during the year—Job P and Job Q. The company uses a plantwide predetermined overhead rate based on machine-hours. At the beginning of the year, it estimated that 4,000 machine-hours would be required for the period’s estimated level of production. Sweeten also estimated $25,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $1.70 per machine-hour.

Because Sweeten has two manufacturing departments—Molding and Fabrication—it is considering replacing its plantwide overhead rate with departmental rates that would also be based on machine-hours. The company gathered the following additional information to enable calculating departmental overhead rates:

| Molding | Fabrication | Total | |

|---|---|---|---|

| Estimated total machine-hours used | 2,500 | 1,500 | 4,000 |

| Estimated total fixed manufacturing overhead | $ 10,000 | $ 15,000 | $ 25,000 |

| Estimated variable manufacturing overhead per machine-hour | $ 1.40 | $ 2.20 |

The direct materials cost, direct labor cost, and machine-hours used for Jobs P and Q are as follows:

| Job P | Job Q | |

|---|---|---|

| Direct materials | $ 13,000 | $ 8,000 |

| Direct labor cost | $ 21,000 | $ 7,500 |

| Actual machine-hours used: | ||

| Molding | 1,700 | 800 |

| Fabrication | 600 | 900 |

| Total | 2,300 | 1,700 |

Sweeten Company had no overapplied or underapplied manufacturing overhead costs during the year.

Required:

For questions 1-8, assume that Sweeten Company uses a plantwide predetermined overhead rate with machine-hours as the allocation base. For questions, 9-15, assume that the company uses predetermined departmental overhead rates with machine-hours as the allocation base in both departments.

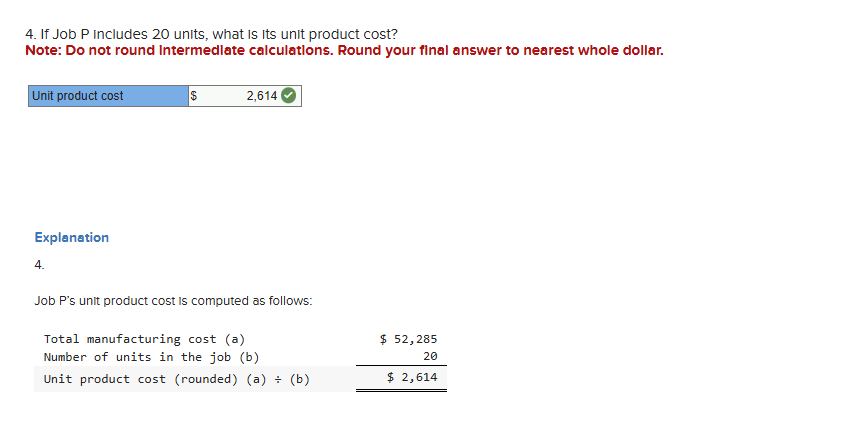

4. [The following information applies to the questions displayed below.]

Sweeten Company had no jobs in progress at the beginning of the year and no beginning inventories. It started, completed, and sold only two jobs during the year—Job P and Job Q. The company uses a plantwide predetermined overhead rate based on machine-hours. At the beginning of the year, it estimated that 4,000 machine-hours would be required for the period’s estimated level of production. Sweeten also estimated $25,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $1.70 per machine-hour.

Because Sweeten has two manufacturing departments—Molding and Fabrication—it is considering replacing its plantwide overhead rate with departmental rates that would also be based on machine-hours. The company gathered the following additional information to enable calculating departmental overhead rates:

| Molding | Fabrication | Total | |

|---|---|---|---|

| Estimated total machine-hours used | 2,500 | 1,500 | 4,000 |

| Estimated total fixed manufacturing overhead | $ 10,000 | $ 15,000 | $ 25,000 |

| Estimated variable manufacturing overhead per machine-hour | $ 1.40 | $ 2.20 |

The direct materials cost, direct labor cost, and machine-hours used for Jobs P and Q are as follows:

| Job P | Job Q | |

|---|---|---|

| Direct materials | $ 13,000 | $ 8,000 |

| Direct labor cost | $ 21,000 | $ 7,500 |

| Actual machine-hours used: | ||

| Molding | 1,700 | 800 |

| Fabrication | 600 | 900 |

| Total | 2,300 | 1,700 |

Sweeten Company had no overapplied or underapplied manufacturing overhead costs during the year.

Required:

For questions 1-8, assume that Sweeten Company uses a plantwide predetermined overhead rate with machine-hours as the allocation base. For questions, 9-15, assume that the company uses predetermined departmental overhead rates with machine-hours as the allocation base in both departments.

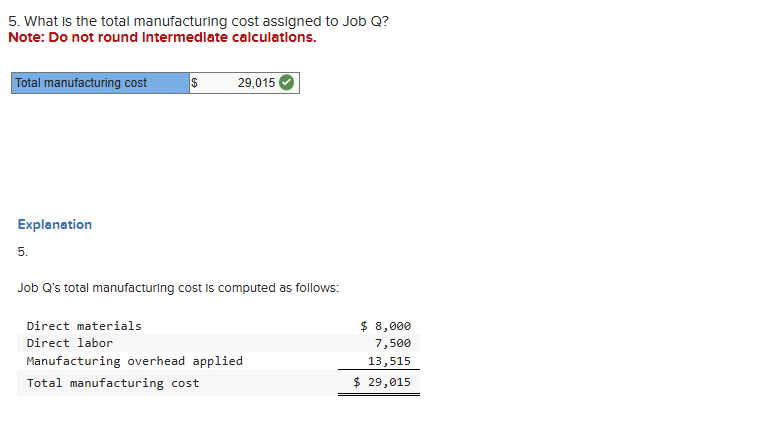

5. [The following information applies to the questions displayed below.]

Sweeten Company had no jobs in progress at the beginning of the year and no beginning inventories. It started, completed, and sold only two jobs during the year—Job P and Job Q. The company uses a plantwide predetermined overhead rate based on machine-hours. At the beginning of the year, it estimated that 4,000 machine-hours would be required for the period’s estimated level of production. Sweeten also estimated $25,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $1.70 per machine-hour.

Because Sweeten has two manufacturing departments—Molding and Fabrication—it is considering replacing its plantwide overhead rate with departmental rates that would also be based on machine-hours. The company gathered the following additional information to enable calculating departmental overhead rates:

| Molding | Fabrication | Total | |

|---|---|---|---|

| Estimated total machine-hours used | 2,500 | 1,500 | 4,000 |

| Estimated total fixed manufacturing overhead | $ 10,000 | $ 15,000 | $ 25,000 |

| Estimated variable manufacturing overhead per machine-hour | $ 1.40 | $ 2.20 |

The direct materials cost, direct labor cost, and machine-hours used for Jobs P and Q are as follows:

| Job P | Job Q | |

|---|---|---|

| Direct materials | $ 13,000 | $ 8,000 |

| Direct labor cost | $ 21,000 | $ 7,500 |

| Actual machine-hours used: | ||

| Molding | 1,700 | 800 |

| Fabrication | 600 | 900 |

| Total | 2,300 | 1,700 |

Sweeten Company had no overapplied or underapplied manufacturing overhead costs during the year.

Required:

For questions 1-8, assume that Sweeten Company uses a plantwide predetermined overhead rate with machine-hours as the allocation base. For questions, 9-15, assume that the company uses predetermined departmental overhead rates with machine-hours as the allocation base in both departments.

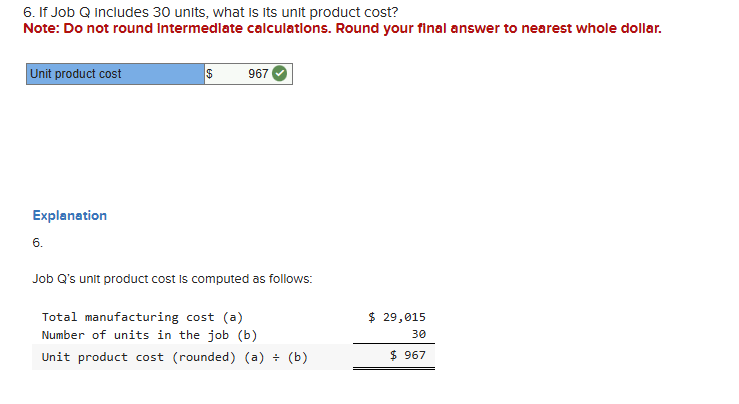

6. [The following information applies to the questions displayed below.]

Sweeten Company had no jobs in progress at the beginning of the year and no beginning inventories. It started, completed, and sold only two jobs during the year—Job P and Job Q. The company uses a plantwide predetermined overhead rate based on machine-hours. At the beginning of the year, it estimated that 4,000 machine-hours would be required for the period’s estimated level of production. Sweeten also estimated $25,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $1.70 per machine-hour.

Because Sweeten has two manufacturing departments—Molding and Fabrication—it is considering replacing its plantwide overhead rate with departmental rates that would also be based on machine-hours. The company gathered the following additional information to enable calculating departmental overhead rates:

| Molding | Fabrication | Total | |

|---|---|---|---|

| Estimated total machine-hours used | 2,500 | 1,500 | 4,000 |

| Estimated total fixed manufacturing overhead | $ 10,000 | $ 15,000 | $ 25,000 |

| Estimated variable manufacturing overhead per machine-hour | $ 1.40 | $ 2.20 |

The direct materials cost, direct labor cost, and machine-hours used for Jobs P and Q are as follows:

| Job P | Job Q | |

|---|---|---|

| Direct materials | $ 13,000 | $ 8,000 |

| Direct labor cost | $ 21,000 | $ 7,500 |

| Actual machine-hours used: | ||

| Molding | 1,700 | 800 |

| Fabrication | 600 | 900 |

| Total | 2,300 | 1,700 |

Sweeten Company had no overapplied or underapplied manufacturing overhead costs during the year.

Required:

For questions 1-8, assume that Sweeten Company uses a plantwide predetermined overhead rate with machine-hours as the allocation base. For questions, 9-15, assume that the company uses predetermined departmental overhead rates with machine-hours as the allocation base in both departments.

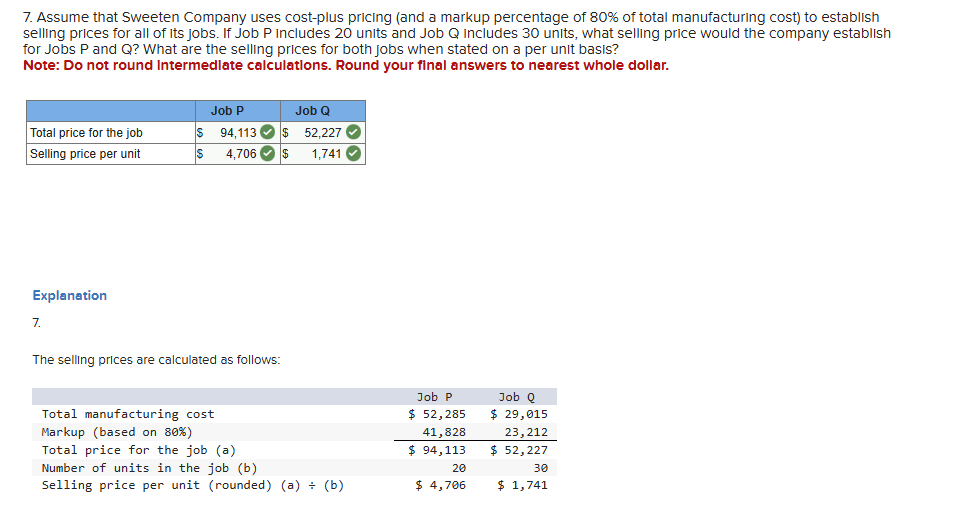

7. [The following information applies to the questions displayed below.]

Sweeten Company had no jobs in progress at the beginning of the year and no beginning inventories. It started, completed, and sold only two jobs during the year—Job P and Job Q. The company uses a plantwide predetermined overhead rate based on machine-hours. At the beginning of the year, it estimated that 4,000 machine-hours would be required for the period’s estimated level of production. Sweeten also estimated $25,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $1.70 per machine-hour.

Because Sweeten has two manufacturing departments—Molding and Fabrication—it is considering replacing its plantwide overhead rate with departmental rates that would also be based on machine-hours. The company gathered the following additional information to enable calculating departmental overhead rates:

| Molding | Fabrication | Total | |

|---|---|---|---|

| Estimated total machine-hours used | 2,500 | 1,500 | 4,000 |

| Estimated total fixed manufacturing overhead | $ 10,000 | $ 15,000 | $ 25,000 |

| Estimated variable manufacturing overhead per machine-hour | $ 1.40 | $ 2.20 |

The direct materials cost, direct labor cost, and machine-hours used for Jobs P and Q are as follows:

| Job P | Job Q | |

|---|---|---|

| Direct materials | $ 13,000 | $ 8,000 |

| Direct labor cost | $ 21,000 | $ 7,500 |

| Actual machine-hours used: | ||

| Molding | 1,700 | 800 |

| Fabrication | 600 | 900 |

| Total | 2,300 | 1,700 |

Sweeten Company had no overapplied or underapplied manufacturing overhead costs during the year.

Required:

For questions 1-8, assume that Sweeten Company uses a plantwide predetermined overhead rate with machine-hours as the allocation base. For questions, 9-15, assume that the company uses predetermined departmental overhead rates with machine-hours as the allocation base in both departments.

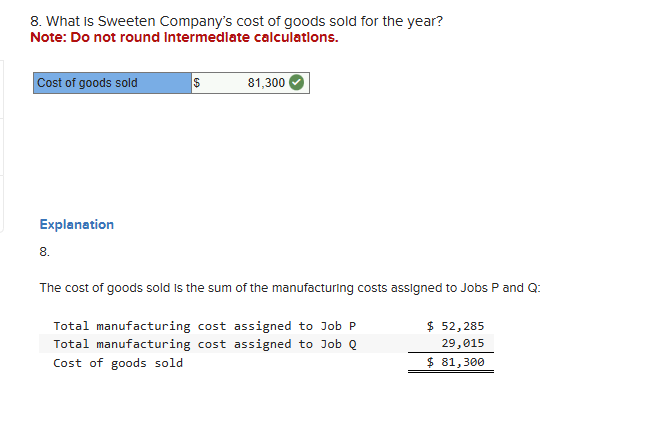

8. [The following information applies to the questions displayed below.]

Sweeten Company had no jobs in progress at the beginning of the year and no beginning inventories. It started, completed, and sold only two jobs during the year—Job P and Job Q. The company uses a plantwide predetermined overhead rate based on machine-hours. At the beginning of the year, it estimated that 4,000 machine-hours would be required for the period’s estimated level of production. Sweeten also estimated $25,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $1.70 per machine-hour.

Because Sweeten has two manufacturing departments—Molding and Fabrication—it is considering replacing its plantwide overhead rate with departmental rates that would also be based on machine-hours. The company gathered the following additional information to enable calculating departmental overhead rates:

| Molding | Fabrication | Total | |

|---|---|---|---|

| Estimated total machine-hours used | 2,500 | 1,500 | 4,000 |

| Estimated total fixed manufacturing overhead | $ 10,000 | $ 15,000 | $ 25,000 |

| Estimated variable manufacturing overhead per machine-hour | $ 1.40 | $ 2.20 |

The direct materials cost, direct labor cost, and machine-hours used for Jobs P and Q are as follows:

| Job P | Job Q | |

|---|---|---|

| Direct materials | $ 13,000 | $ 8,000 |

| Direct labor cost | $ 21,000 | $ 7,500 |

| Actual machine-hours used: | ||

| Molding | 1,700 | 800 |

| Fabrication | 600 | 900 |

| Total | 2,300 | 1,700 |

Sweeten Company had no overapplied or underapplied manufacturing overhead costs during the year.

Required:

For questions 1-8, assume that Sweeten Company uses a plantwide predetermined overhead rate with machine-hours as the allocation base. For questions, 9-15, assume that the company uses predetermined departmental overhead rates with machine-hours as the allocation base in both departments.

9. [The following information applies to the questions displayed below.]

Sweeten Company had no jobs in progress at the beginning of the year and no beginning inventories. It started, completed, and sold only two jobs during the year—Job P and Job Q. The company uses a plantwide predetermined overhead rate based on machine-hours. At the beginning of the year, it estimated that 4,000 machine-hours would be required for the period’s estimated level of production. Sweeten also estimated $25,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $1.70 per machine-hour.

Because Sweeten has two manufacturing departments—Molding and Fabrication—it is considering replacing its plantwide overhead rate with departmental rates that would also be based on machine-hours. The company gathered the following additional information to enable calculating departmental overhead rates:

| Molding | Fabrication | Total | |

|---|---|---|---|

| Estimated total machine-hours used | 2,500 | 1,500 | 4,000 |

| Estimated total fixed manufacturing overhead | $ 10,000 | $ 15,000 | $ 25,000 |

| Estimated variable manufacturing overhead per machine-hour | $ 1.40 | $ 2.20 |

The direct materials cost, direct labor cost, and machine-hours used for Jobs P and Q are as follows:

| Job P | Job Q | |

|---|---|---|

| Direct materials | $ 13,000 | $ 8,000 |

| Direct labor cost | $ 21,000 | $ 7,500 |

| Actual machine-hours used: | ||

| Molding | 1,700 | 800 |

| Fabrication | 600 | 900 |

| Total | 2,300 | 1,700 |

Sweeten Company had no overapplied or underapplied manufacturing overhead costs during the year.

Required:

For questions 1-8, assume that Sweeten Company uses a plantwide predetermined overhead rate with machine-hours as the allocation base. For questions, 9-15, assume that the company uses predetermined departmental overhead rates with machine-hours as the allocation base in both departments.

10. [The following information applies to the questions displayed below.]

Sweeten Company had no jobs in progress at the beginning of the year and no beginning inventories. It started, completed, and sold only two jobs during the year—Job P and Job Q. The company uses a plantwide predetermined overhead rate based on machine-hours. At the beginning of the year, it estimated that 4,000 machine-hours would be required for the period’s estimated level of production. Sweeten also estimated $25,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $1.70 per machine-hour.

Because Sweeten has two manufacturing departments—Molding and Fabrication—it is considering replacing its plantwide overhead rate with departmental rates that would also be based on machine-hours. The company gathered the following additional information to enable calculating departmental overhead rates:

| Molding | Fabrication | Total | |

|---|---|---|---|

| Estimated total machine-hours used | 2,500 | 1,500 | 4,000 |

| Estimated total fixed manufacturing overhead | $ 10,000 | $ 15,000 | $ 25,000 |

| Estimated variable manufacturing overhead per machine-hour | $ 1.40 | $ 2.20 |

The direct materials cost, direct labor cost, and machine-hours used for Jobs P and Q are as follows:

| Job P | Job Q | |

|---|---|---|

| Direct materials | $ 13,000 | $ 8,000 |

| Direct labor cost | $ 21,000 | $ 7,500 |

| Actual machine-hours used: | ||

| Molding | 1,700 | 800 |

| Fabrication | 600 | 900 |

| Total | 2,300 | 1,700 |

Sweeten Company had no overapplied or underapplied manufacturing overhead costs during the year.

Required:

For questions 1-8, assume that Sweeten Company uses a plantwide predetermined overhead rate with machine-hours as the allocation base. For questions, 9-15, assume that the company uses predetermined departmental overhead rates with machine-hours as the allocation base in both departments.

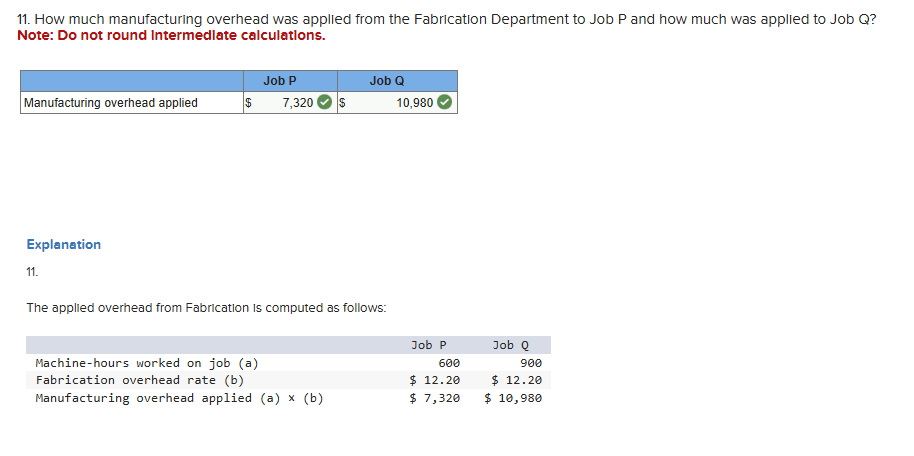

11. [The following information applies to the questions displayed below.]

Sweeten Company had no jobs in progress at the beginning of the year and no beginning inventories. It started, completed, and sold only two jobs during the year—Job P and Job Q. The company uses a plantwide predetermined overhead rate based on machine-hours. At the beginning of the year, it estimated that 4,000 machine-hours would be required for the period’s estimated level of production. Sweeten also estimated $25,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $1.70 per machine-hour.

Because Sweeten has two manufacturing departments—Molding and Fabrication—it is considering replacing its plantwide overhead rate with departmental rates that would also be based on machine-hours. The company gathered the following additional information to enable calculating departmental overhead rates:

| Molding | Fabrication | Total | |

|---|---|---|---|

| Estimated total machine-hours used | 2,500 | 1,500 | 4,000 |

| Estimated total fixed manufacturing overhead | $ 10,000 | $ 15,000 | $ 25,000 |

| Estimated variable manufacturing overhead per machine-hour | $ 1.40 | $ 2.20 |

The direct materials cost, direct labor cost, and machine-hours used for Jobs P and Q are as follows:

| Job P | Job Q | |

|---|---|---|

| Direct materials | $ 13,000 | $ 8,000 |

| Direct labor cost | $ 21,000 | $ 7,500 |

| Actual machine-hours used: | ||

| Molding | 1,700 | 800 |

| Fabrication | 600 | 900 |

| Total | 2,300 | 1,700 |

Sweeten Company had no overapplied or underapplied manufacturing overhead costs during the year.

Required:

For questions 1-8, assume that Sweeten Company uses a plantwide predetermined overhead rate with machine-hours as the allocation base. For questions, 9-15, assume that the company uses predetermined departmental overhead rates with machine-hours as the allocation base in both departments.

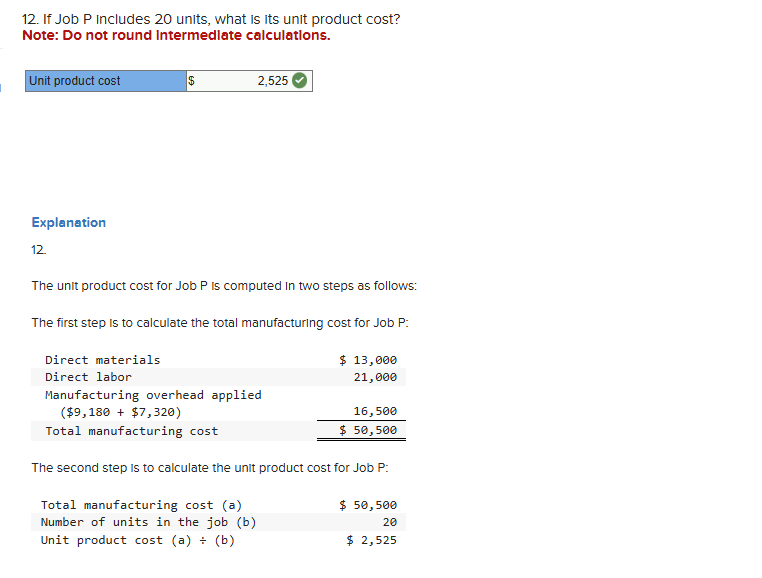

12. [The following information applies to the questions displayed below.]

Sweeten Company had no jobs in progress at the beginning of the year and no beginning inventories. It started, completed, and sold only two jobs during the year—Job P and Job Q. The company uses a plantwide predetermined overhead rate based on machine-hours. At the beginning of the year, it estimated that 4,000 machine-hours would be required for the period’s estimated level of production. Sweeten also estimated $25,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $1.70 per machine-hour.

Because Sweeten has two manufacturing departments—Molding and Fabrication—it is considering replacing its plantwide overhead rate with departmental rates that would also be based on machine-hours. The company gathered the following additional information to enable calculating departmental overhead rates:

| Molding | Fabrication | Total | |

|---|---|---|---|

| Estimated total machine-hours used | 2,500 | 1,500 | 4,000 |

| Estimated total fixed manufacturing overhead | $ 10,000 | $ 15,000 | $ 25,000 |

| Estimated variable manufacturing overhead per machine-hour | $ 1.40 | $ 2.20 |

The direct materials cost, direct labor cost, and machine-hours used for Jobs P and Q are as follows:

| Job P | Job Q | |

|---|---|---|

| Direct materials | $ 13,000 | $ 8,000 |

| Direct labor cost | $ 21,000 | $ 7,500 |

| Actual machine-hours used: | ||

| Molding | 1,700 | 800 |

| Fabrication | 600 | 900 |

| Total | 2,300 | 1,700 |

Sweeten Company had no overapplied or underapplied manufacturing overhead costs during the year.

Required:

For questions 1-8, assume that Sweeten Company uses a plantwide predetermined overhead rate with machine-hours as the allocation base. For questions, 9-15, assume that the company uses predetermined departmental overhead rates with machine-hours as the allocation base in both departments.

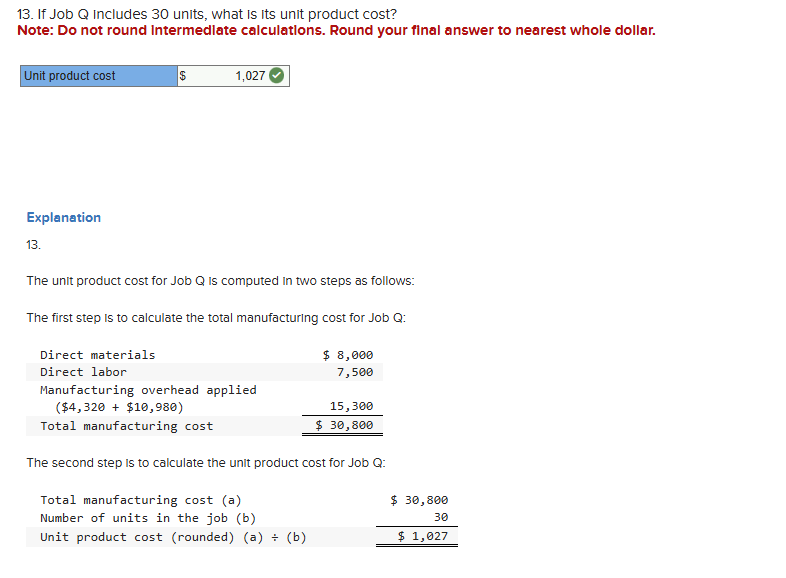

13. [The following information applies to the questions displayed below.]

Sweeten Company had no jobs in progress at the beginning of the year and no beginning inventories. It started, completed, and sold only two jobs during the year—Job P and Job Q. The company uses a plantwide predetermined overhead rate based on machine-hours. At the beginning of the year, it estimated that 4,000 machine-hours would be required for the period’s estimated level of production. Sweeten also estimated $25,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $1.70 per machine-hour.

Because Sweeten has two manufacturing departments—Molding and Fabrication—it is considering replacing its plantwide overhead rate with departmental rates that would also be based on machine-hours. The company gathered the following additional information to enable calculating departmental overhead rates:

| Molding | Fabrication | Total | |

|---|---|---|---|

| Estimated total machine-hours used | 2,500 | 1,500 | 4,000 |

| Estimated total fixed manufacturing overhead | $ 10,000 | $ 15,000 | $ 25,000 |

| Estimated variable manufacturing overhead per machine-hour | $ 1.40 | $ 2.20 |

The direct materials cost, direct labor cost, and machine-hours used for Jobs P and Q are as follows:

| Job P | Job Q | |

|---|---|---|

| Direct materials | $ 13,000 | $ 8,000 |

| Direct labor cost | $ 21,000 | $ 7,500 |

| Actual machine-hours used: | ||

| Molding | 1,700 | 800 |

| Fabrication | 600 | 900 |

| Total | 2,300 | 1,700 |

Sweeten Company had no overapplied or underapplied manufacturing overhead costs during the year.

Required:

For questions 1-8, assume that Sweeten Company uses a plantwide predetermined overhead rate with machine-hours as the allocation base. For questions, 9-15, assume that the company uses predetermined departmental overhead rates with machine-hours as the allocation base in both departments.[The following information applies to the questions displayed below.]

Sweeten Company had no jobs in progress at the beginning of the year and no beginning inventories. It started, completed, and sold only two jobs during the year—Job P and Job Q. The company uses a plantwide predetermined overhead rate based on machine-hours. At the beginning of the year, it estimated that 4,000 machine-hours would be required for the period’s estimated level of production. Sweeten also estimated $25,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $1.70 per machine-hour.

Because Sweeten has two manufacturing departments—Molding and Fabrication—it is considering replacing its plantwide overhead rate with departmental rates that would also be based on machine-hours. The company gathered the following additional information to enable calculating departmental overhead rates:

| Molding | Fabrication | Total | |

|---|---|---|---|

| Estimated total machine-hours used | 2,500 | 1,500 | 4,000 |

| Estimated total fixed manufacturing overhead | $ 10,000 | $ 15,000 | $ 25,000 |

| Estimated variable manufacturing overhead per machine-hour | $ 1.40 | $ 2.20 |

The direct materials cost, direct labor cost, and machine-hours used for Jobs P and Q are as follows:

| Job P | Job Q | |

|---|---|---|

| Direct materials | $ 13,000 | $ 8,000 |

| Direct labor cost | $ 21,000 | $ 7,500 |

| Actual machine-hours used: | ||

| Molding | 1,700 | 800 |

| Fabrication | 600 | 900 |

| Total | 2,300 | 1,700 |

Sweeten Company had no overapplied or underapplied manufacturing overhead costs during the year.

Required:

For questions 1-8, assume that Sweeten Company uses a plantwide predetermined overhead rate with machine-hours as the allocation base. For questions, 9-15, assume that the company uses predetermined departmental overhead rates with machine-hours as the allocation base in both departments.

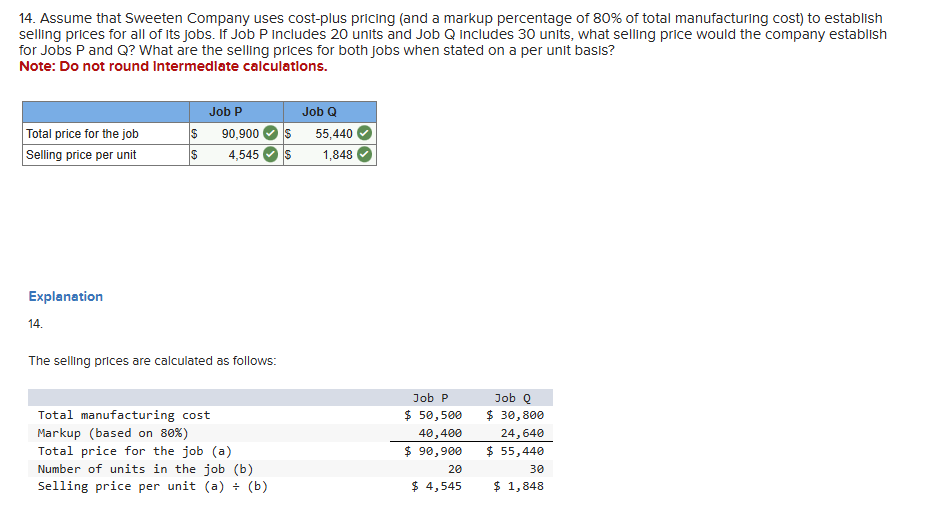

14. [The following information applies to the questions displayed below.]

Sweeten Company had no jobs in progress at the beginning of the year and no beginning inventories. It started, completed, and sold only two jobs during the year—Job P and Job Q. The company uses a plantwide predetermined overhead rate based on machine-hours. At the beginning of the year, it estimated that 4,000 machine-hours would be required for the period’s estimated level of production. Sweeten also estimated $25,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $1.70 per machine-hour.

Because Sweeten has two manufacturing departments—Molding and Fabrication—it is considering replacing its plantwide overhead rate with departmental rates that would also be based on machine-hours. The company gathered the following additional information to enable calculating departmental overhead rates:

| Molding | Fabrication | Total | |

|---|---|---|---|

| Estimated total machine-hours used | 2,500 | 1,500 | 4,000 |

| Estimated total fixed manufacturing overhead | $ 10,000 | $ 15,000 | $ 25,000 |

| Estimated variable manufacturing overhead per machine-hour | $ 1.40 | $ 2.20 |

The direct materials cost, direct labor cost, and machine-hours used for Jobs P and Q are as follows:

| Job P | Job Q | |

|---|---|---|

| Direct materials | $ 13,000 | $ 8,000 |

| Direct labor cost | $ 21,000 | $ 7,500 |

| Actual machine-hours used: | ||

| Molding | 1,700 | 800 |

| Fabrication | 600 | 900 |

| Total | 2,300 | 1,700 |

Sweeten Company had no overapplied or underapplied manufacturing overhead costs during the year.

Required:

For questions 1-8, assume that Sweeten Company uses a plantwide predetermined overhead rate with machine-hours as the allocation base. For questions, 9-15, assume that the company uses predetermined departmental overhead rates with machine-hours as the allocation base in both departments.

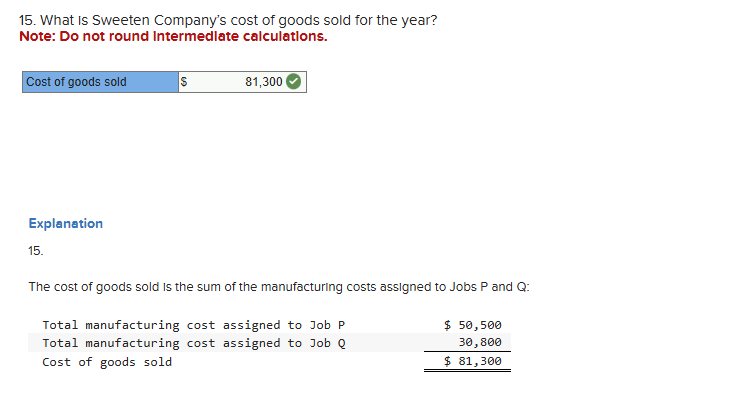

15. [The following information applies to the questions displayed below.]

Sweeten Company had no jobs in progress at the beginning of the year and no beginning inventories. It started, completed, and sold only two jobs during the year—Job P and Job Q. The company uses a plantwide predetermined overhead rate based on machine-hours. At the beginning of the year, it estimated that 4,000 machine-hours would be required for the period’s estimated level of production. Sweeten also estimated $25,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $1.70 per machine-hour.

Because Sweeten has two manufacturing departments—Molding and Fabrication—it is considering replacing its plantwide overhead rate with departmental rates that would also be based on machine-hours. The company gathered the following additional information to enable calculating departmental overhead rates:

| Molding | Fabrication | Total | |

|---|---|---|---|

| Estimated total machine-hours used | 2,500 | 1,500 | 4,000 |

| Estimated total fixed manufacturing overhead | $ 10,000 | $ 15,000 | $ 25,000 |

| Estimated variable manufacturing overhead per machine-hour | $ 1.40 | $ 2.20 |

The direct materials cost, direct labor cost, and machine-hours used for Jobs P and Q are as follows:

| Job P | Job Q | |

|---|---|---|

| Direct materials | $ 13,000 | $ 8,000 |

| Direct labor cost | $ 21,000 | $ 7,500 |

| Actual machine-hours used: | ||

| Molding | 1,700 | 800 |

| Fabrication | 600 | 900 |

| Total | 2,300 | 1,700 |

Sweeten Company had no overapplied or underapplied manufacturing overhead costs during the year.

Required:

For questions 1-8, assume that Sweeten Company uses a plantwide predetermined overhead rate with machine-hours as the allocation base. For questions, 9-15, assume that the company uses predetermined departmental overhead rates with machine-hours as the allocation base in both departments.