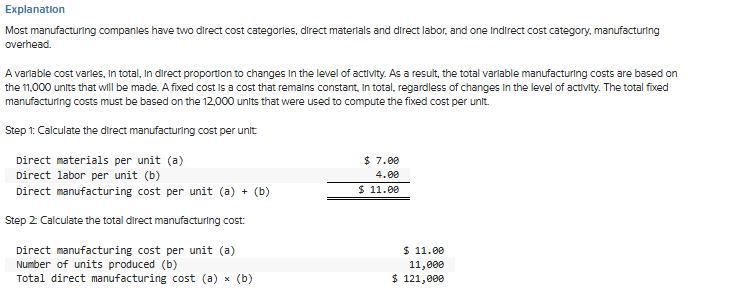

1.A company’s relevant range of production is 10,000 to 15,000 units. When it produces and sells 12,000 units, its unit costs are as follows:

| Amount per Unit | |

|---|---|

| Direct materials | $ 7.00 |

| Direct labor | $ 4.00 |

| Variable manufacturing overhead | $ 1.50 |

| Fixed manufacturing overhead | $ 5.00 |

| Fixed selling expense | $ 3.50 |

| Fixed administrative expense | $ 2.00 |

| Sales commissions | $ 1.00 |

| Variable administrative expense | $ 0.50 |

If 11,000 units are produced, what is the total amount of direct manufacturing costs incurred to support this level of production?

A) $121,000

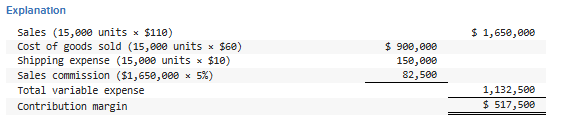

2.A merchandiser plans to sell 15,000 units next month at a selling price of $110 per unit. It also gathered the following cost estimates for next month:

| Cost | Cost Formula |

|---|---|

| Cost of goods sold | $60 per unit sold |

| Advertising expense | $150,000 per month |

| Depreciation expense | $70,000 per month |

| Shipping expense | $100,000 per month + $10 per unit sold |

| Administrative salaries | $50,000 per month |

| Sales commissions | 5% of sales |

| Insurance expense | $15,000 per month |

What is the estimated total contribution margin for next month?

A) $517,500

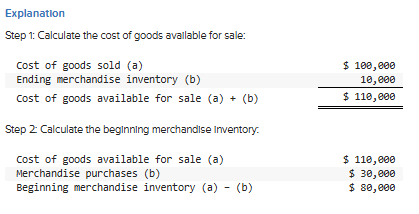

3.If the cost of goods sold is $100,000, sales are $200,000, merchandise purchases are $30,000, and ending merchandise inventory is $10,000, then the beginning merchandise inventory must be:

A) $80,000.

4.A unit product cost includes:

A) Actual direct labor cost used by the job.

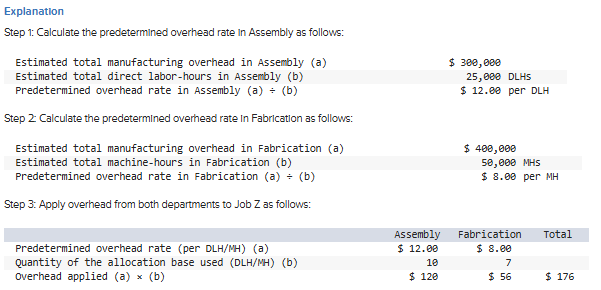

5.Assume a company has two manufacturing departments – Assembly and Fabrication. The company considers all of its manufacturing overhead costs to be fixed costs. The first set of data below is budgeted data for the company as a whole that was estimated at the beginning of the year. The second set of data below is actual data for the company as a whole that was derived at the end of the year. The third set of data relates to one particular job completed during the year– Job Z.

| Budgeted Data | Assembly | Fabrication |

|---|---|---|

| Manufacturing overhead costs | $ 300,000 | $ 400,000 |

| Direct labor hours | 25,000 | 15,000 |

| Machine hours | 10,000 | 50,000 |

| Actual Data | Assembly | Fabrication |

|---|---|---|

| Manufacturing overhead costs | $ 330,000 | $ 380,000 |

| Direct labor hours | 27,000 | 16,000 |

| Machine hours | 10,500 | 48,000 |

| Job Z | Assembly | Fabrication | ||

|---|---|---|---|---|

| Direct labor hours | 10 | hours | 2 | hours |

| Machine hours | 1 | hour | 7 | hours |

Assume the company uses departmental predetermined overhead rates. It uses direct labor-hours as the allocation base in Assembly and machine-hours as the allocation base in Fabrication. How much manufacturing overhead would be applied from both departments to Job Z?

A) $176

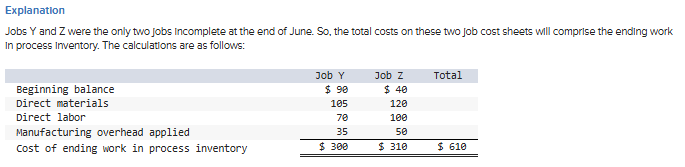

6.Assume a company worked on four jobs during June: Jobs W, X, Y, and Z. At the end of June, the job cost sheets for these four jobs contained the following data:

| Job W | Job X | Job Y | Job Z | |

|---|---|---|---|---|

| Beginning balance | $ 80 | $ 120 | $ 90 | $ 40 |

| Charged to the jobs during June: | ||||

| Direct materials | $ 145 | $ 80 | $ 105 | $ 120 |

| Direct labor | $ 90 | $ 50 | $ 70 | $ 100 |

| Manufacturing overhead applied | $ 45 | $ 25 | $ 35 | $ 50 |

| Units completed | 80 | 100 | 0 | 0 |

| Units sold during June | 40 | 100 | 0 | 0 |

Jobs W and X were completed during June. Jobs Y and Z were incomplete at the end of June. There was no finished goods inventory on June 1 and the company’s total manufacturing overhead always applied equals its total actual manufacturing overhead.

The work in process inventory balance at the end of June is closest to:

A) $610.

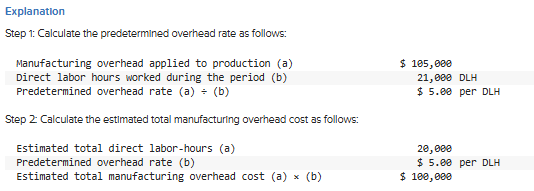

7.Assume the following:

- Estimated direct labor hours used to calculate the predetermined overhead rate = 20,000

- The manufacturing overhead applied to production = $105,000

- The total direct labor hours actually worked during the period = 21,000.

What is the estimated total manufacturing overhead cost for the period?

A) $100,000

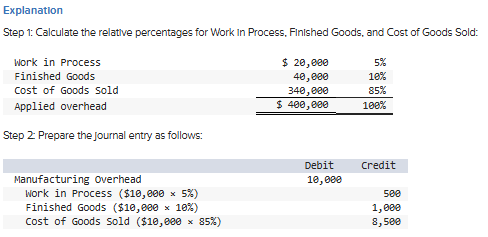

8.At the end of the year, a company’s applied overhead is distributed among its inventory accounts and cost of goods sold as follows:

| Work in Process | $ 20,000 |

|---|---|

| Finished Goods | 40,000 |

| Cost of Goods Sold | 340,000 |

| Applied overhead | $ 400,000 |

If the company has $10,000 of overapplied overhead and it closes this amount proportionally to Work in Process, Finished Goods, and Cost of Goods Sold, then which of the following statements is true?

A) The entry to dispose of the overapplied overhead will include a credit to Cost of Goods Sold for $8,500.

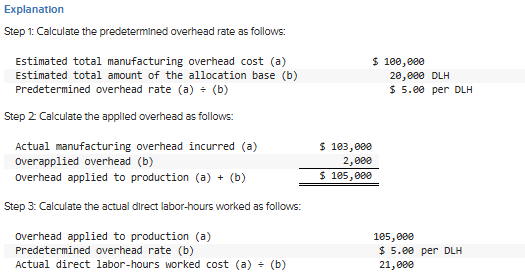

9.Assume the following:

- Estimated direct labor hours used to calculate the predetermined overhead rate = 20,000

- The estimated total manufacturing overhead cost = $100,000

- The actual manufacturing overhead costs incurred during the period = $103,000

- Manufacturing overhead is overapplied by $2,000.

What is the actual number of direct labor-hours worked during the period?

A) 21,000

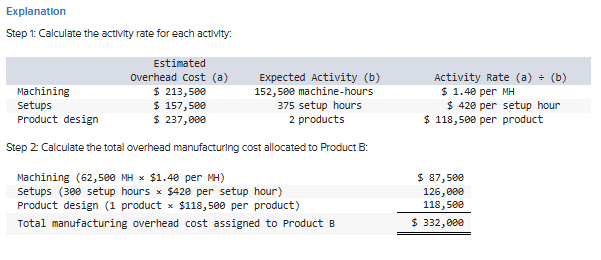

10.In its first year of operations a company produced and sold 70,000 units of Product A and 17,500 units of Product B. Additional information relating to the company’s only two products is shown below:

| Product A | Product B | Total | |

|---|---|---|---|

| Direct materials | $ 436,300 | $ 251,700 | $ 688,000 |

| Direct labor | $ 200,000 | $ 104,000 | $ 304,000 |

The company’s direct labor wage rate is $20 per hour. It created an activity-based costing system that allocated all of its manufacturing overhead costs to three activities as follows:

| Activity Cost Pool (and Activity Measure) | Manufacturing Overhead | Activity | ||

|---|---|---|---|---|

| Product A | Product B | Total | ||

| Machining (machine-hours) | $ 213,500 | 90,000 | 62,500 | 152,500 |

| Setups (setup hours) | 157,500 | 75 | 300 | 375 |

| Product design (number of products) | 237,000 | 1 | 1 | 2 |

| Total manufacturing overhead cost | $ 608,000 | |||

The company’s activity-based costing system would allocate how much manufacturing overhead to Product B?

A) $332,000

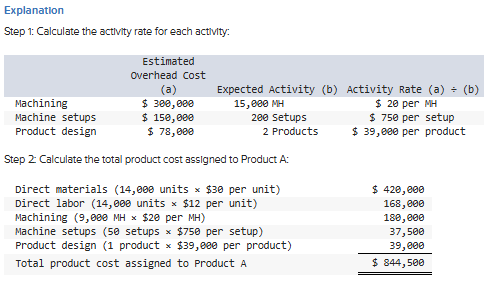

11.Assume a company produces and sells only two products—14,000 units of Product A and 6,000 units of Product B. Product A’s direct materials and direct labor costs per unit are $30 and $12, respectively. Product B’s direct materials and direct labor costs per unit are $34 and $15, respectively. The company is considering implementing an activity-based costing (ABC) system that allocates all of its manufacturing overhead to three cost pools. The following additional information is available for the company as a whole and for Products A and B:

| Activity Cost Pool | Activity Measure | Estimated Overhead Cost | Expected Activity | |

|---|---|---|---|---|

| Machining | Machine-hours | $ 300,000 | 15,000 | MH |

| Machine setups | Number of setups | $ 150,000 | 200 | Setups |

| Product design | Number of products | $ 78,000 | 2 | Products |

| Activity Measure | Product A | Product B |

|---|---|---|

| Machine-hours | 9,000 | 6,000 |

| Number of setups | 50 | 150 |

| Number of products | 1 | 1 |

Using the ABC system, what is the total product cost assigned to Product A?

A) $844,500

12.A company produces numerous blends of coffee, two of which are known as the French blend and the Italian blend. The company’s ABC system divides its total manufacturing overhead of $1,982,500 into four activity cost pools as shown below.

| Activity | Activity Measure | Expected Activity | Estimated Cost | |

|---|---|---|---|---|

| Purchasing | Purchase orders | 1,500 | orders | $ 330,000 |

| Materials handling | Number of setups | 1,800 | setups | $ 540,000 |

| Quality control | Number of batches | 600 | batches | $ 210,000 |

| Roasting | Roasting hours | 95,000 | hours | $ 902,500 |

Data regarding production of the French and Italian blends are as follows:

| French Blend | Italian Blend | |||

|---|---|---|---|---|

| Expected sales | 100,000 | pounds | 5,000 | pounds |

| Batch size | 10,000 | pounds | 1,250 | pounds |

| Setups | 3 | per batch | 3 | per batch |

| Purchase order size | 20,000 | pounds | 500 | pounds |

| Roasting time per 100 pounds | 0.5 | hours | 0.5 | hours |

Assume the company uses a plantwide predetermined overhead rate based on roasting hours. The plantwide predetermined overhead rate is closest to:

A) $20.87.

13.Using the FIFO method, the cost per equivalent unit is calculated using which of the following equations?

A) Cost added during the period ÷ Equivalent units of production

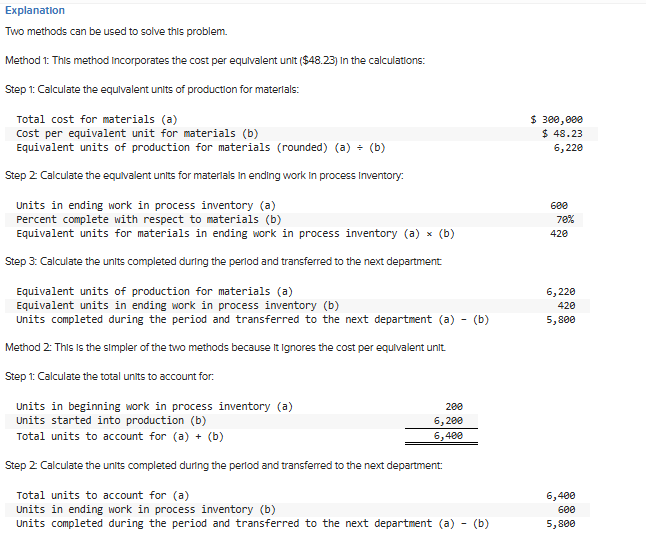

14.Assume the following information:

| Milling Department | Units | Percent Complete | |

|---|---|---|---|

| Materials | Conversion | ||

| Beginning work in process inventory | 200 | 40% | 30% |

| Units started into production during March | 6,200 | ||

| Units completed during the period and transferred to the next department | ?question mark% | 100% | 100% |

| Ending work in process inventory | 600 | 70% | 60% |

| Milling Department | Materials | Conversion |

|---|---|---|

| Cost of beginning work in process inventory | $ 10,000 | $ 15,000 |

| Costs added during the period | 290,000 | 385,000 |

| Total cost | $ 300,000 | $ 400,000 |

If the cost per equivalent unit for materials is $48.23 using the weighted-average method, then the number of units completed during the period and transferred to the next department is closest to:

A) 5,800 units.

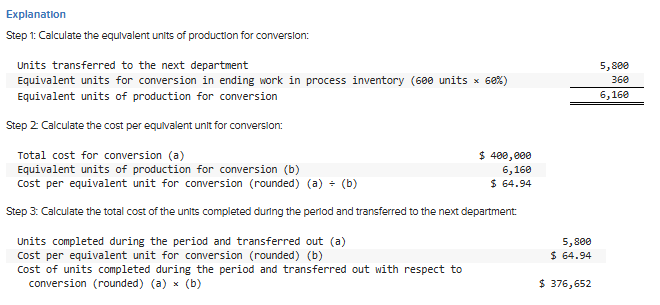

15.Assume the following information:

| Milling Department | Units | Percent Complete | |

|---|---|---|---|

| Materials | Conversion | ||

| Beginning work in process inventory | 200 | 40% | 30% |

| Units started into production during March | 6,200 | ||

| Units completed during the period and transferred to the next department | 5,800 | 100% | 100% |

| Ending work in process inventory | 600 | 70% | 60% |

| Milling Department | Materials | Conversion |

|---|---|---|

| Cost of beginning work in process inventory | $ 10,000 | $ 15,000 |

| Costs added during the period | 290,000 | 385,000 |

| Total cost | $ 300,000 | $ 400,000 |

Using the weighted-average method, the total cost of the units completed during the period and transferred out to the next department with respect to conversion is closest to:

A) $376,652.

16.Which of the following statements is true?

A) Contribution margin − fixed expenses = net operating income

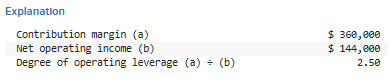

17.Assume the following information:

| Amount | Per Unit | |

|---|---|---|

| Sales | $ 600,000 | $ 40 |

| Contribution margin | $ 360,000 | $ 24 |

| Net operating income | $ 144,000 |

What is the degree of operating leverage?

A) 2.50

18.The contribution margin ratio equals:

A) Contribution margin ÷ sales.

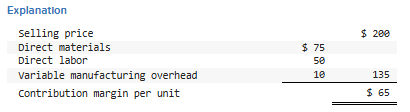

19.Assume the following information for a company that produced and sold 10,000 units during its first year of operations:

| Per Unit | Per Year | |

|---|---|---|

| Selling price | $ 200 | |

| Direct materials | $ 75 | |

| Direct labor | $ 50 | |

| Variable manufacturing overhead | $ 10 | |

| Fixed manufacturing overhead | $ 300,000 |

Using variable costing and based solely on the information provided, what is the company’s contribution margin per unit?

A) $65

20.Which of the following statements is false?

A) Absorption costing treats fixed manufacturing overhead as a period cost.

21.In variable costing, a complete definition of unit product cost includes:

A) Direct materials, direct labor, and variable manufacturing overhead.

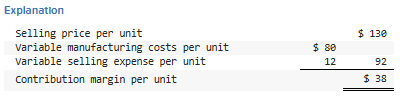

22.Assume that a company sells only one product for a price of $130 per unit. The company’s variable manufacturing costs are $80 per unit, its fixed manufacturing overhead is $24 per unit, and its variable selling expense is $12 per unit. Based solely on the information given, what is the company’s contribution margin per unit under variable costing?

A) $38

23.Which of the following statements is false with respect to a cash budget?

A) It excludes dividends because they are subtracted from retained earnings on the balance sheet.

24.Which of the following statements is true?

A) Control involves gathering feedback that enables organizations to make modifications as circumstances change.

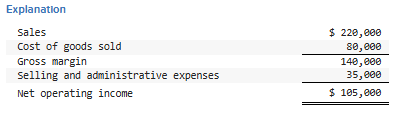

25.Assume a merchandising company provides the following information from its master budget for the month of May:

| Sales | $ 220,000 |

|---|---|

| Cost of goods sold | $ 80,000 |

| Cash paid for merchandise purchases | $ 75,000 |

| Selling and administrative expenses | $ 35,000 |

| Cash paid for selling and administrative expenses | $ 28,000 |

What is the budgeted net operating income?

A) $105,000

26.Which of the following estimates is not used in preparing a sales budget including a schedule of expected cash collections?

A) The number of units produced

27.A planning budget is usually prepared:

A) before the period begins.

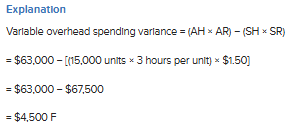

28.Assume the following:

- The variable portion of the predetermined overhead rate is $1.50 per direct labor-hour.

- The standard labor-hours allowed per unit of finished goods is 3 hours.

- The actual quantity of labor hours worked during the period was 44,000 hours.

- The total actual variable manufacturing overhead cost for the period was $63,000.

- The company produced 15,000 units of finished goods during the period.

What is the variable overhead spending variance?

A) $4,500 F

29.Assume that a company provided the following cost formulas for three of its expenses (where q refers to the number of hours worked):

| Rent (fixed) | $ 3,000 |

|---|---|

| Supplies (variable) | $ 4.00q |

| Utilities (mixed) | $ 150 + $ 0.75q |

The company’s planned level of activity was 2,000 hours and its actual level of activity was 1,900 hours. How much rent expense would be included in the flexible budget?

A) $3,000

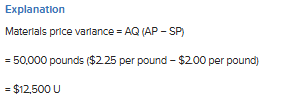

30.Assume the following:

- The standard price per pound is $2.00.

- The standard quantity of pounds allowed per unit of finished goods is 4 pounds.

- The actual quantity of materials purchased and used in production is 50,000 pounds.

- The actual purchase price per pound of materials was $2.25.

- The company produced 13,000 units of finished goods during the period.

What is the materials price variance?

A) $12,500 U

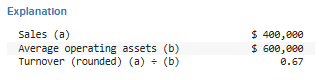

31.Assume a company reported the following results:

| Sales | $ 400,000 |

|---|---|

| Variable expenses | 260,000 |

| Contribution margin | 140,000 |

| Fixed expenses | 40,000 |

| Net operating income | $ 100,000 |

| Average operating assets | $ 600,000 |

The turnover is closest to:

A) 0.67

32.A manager of a profit center is most likely to be evaluated using a:

A) properly formatted segmented income statement.

33.Assume a company reported the following results:

| Sales | $ 400,000 |

|---|---|

| Variable expenses | 260,000 |

| Contribution margin | 140,000 |

| Fixed expenses | 40,000 |

| Net operating income | $ 100,000 |

| Average operating assets | $ 600,000 |

If the company’s minimum required rate of return on average operating assets is 16%, its residual income would be:

A) $4,000.

34.Which of the following measures would most likely appear in the balanced scorecard of a company pursuing a product leadership strategy focused on “offering more innovative and higher quality products than our competitors”?

A) Number of new products designed

35.Which of the following should be ignored when making decisions?

A) Sunk costs

36.Which of the following costs is not relevant when deciding whether to keep or replace a piece of equipment?

A) The original cost of the asset that would be replaced.

37.Assume a manufacturing company is deciding whether to accept or reject a special order opportunity. Which of the following statements is true?

A) The financial analysis should include the incremental costs incurred to fulfill the order.

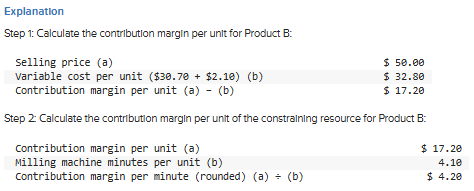

38.Assume a company makes four products (A, B, C, and D) in a single facility. Data concerning these products appear below:

| Product A | Product B | Product C | Product D | |

|---|---|---|---|---|

| Selling price per unit | $ 42.30 | $ 50.00 | $ 37.60 | $ 33.50 |

| Variable manufacturing cost per unit | $ 20.80 | $ 30.70 | $ 21.00 | $ 19.90 |

| Variable selling cost per unit | $ 2.70 | $ 2.10 | $ 1.00 | $ 2.40 |

| Milling machine minutes per unit | 3.30 | 4.10 | 2.60 | 1.30 |

| Monthly demand in units | 1,000 | 4,000 | 3,000 | 3,000 |

The milling machines are the constraint in the production facility. A total of 14,000 minutes is available per month on these machines. The contribution margin per unit of the constraining resource for Product B is closest to:

A) $4.20.

39.A company’s cost of capital is:

A) the average rate of return it must pay to its long-term creditors and shareholders for the use of their funds.

40.Assume the following information for three investment proposals:

| Proposal A | Proposal B | Proposal C | |

|---|---|---|---|

| Investment required | $ (200,000) | $ (275,000) | $ (350,000) |

| Present value of cash inflows | 220,000 | 335,000 | 420,000 |

| Net present value | $ 20,000 | $ 60,000 | $ 70,000 |

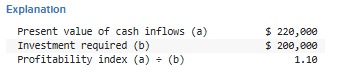

What is the profitability index for Proposal A?

A) 1.10

41.Which of the following capital budgeting methods considers cash flows, but not the time value of money?

A) The payback method

42.Which of the following is not an example of a typical capital budgeting decision?

A) The decision to reduce or maintain this year’s advertising budget.

43.Assume a company sold a piece of equipment that had an original cost of $500,000 and accumulated depreciation of $300,000. The cash proceeds from the sale were $220,000. The gain on the sale was $20,000. Based solely on the information provided, the company’s net cash provided by (used in) investing activities would be:

A) $220,000.

44.Assume a merchandising company reported cost of goods sold of $100,000. Its inventory account balance decreased by $12,000 during the period and its accounts payable balance decreased by $5,000 during the period. The cash paid inventory purchases would be:

A) $93,000.

45.Which of the following cash flows relates to a company’s investing activities?

A) Collecting the principal on a loan to another entity

46.Which of the following statements is true when computing the net cash provided by (used in) operating activities using the indirect method?

A) If the inventory balance decreases during the period, the amount of the decrease is added to net income.

47.Assume a company provided the following information:

| Net income | $ 120,000 |

|---|---|

| Number of common shares outstanding, beginning of the year | 50,000 |

| Number of common shares outstanding, end of the year | 58,000 |

The earnings per share is closest to:

A) $2.22.

48.The current ratio is calculated using which of the following formulas?

A) Current assets ÷ Current liabilities

49.Assume a company provided the following information:

| Net income | $ 120,000 |

|---|---|

| Stockholders’ equity, beginning of the year | $ 475,000 |

| Stockholders’ equity, end of the year | $ 525,000 |

The return on equity is closest to:

A) 24.0%.

50.Assume a company is preparing a sales trend analysis. The total sales in the base year was $800,000. The total sales during the next year were $960,000. The trend analysis would report the next year’s sales as a percent of base year sales closest to:

A) 120.0%.